Introduction

In April 2026, investing in mutual funds is easier than ever. With just a few taps on your smartphone, you can start your investment journey. But before you click “Invest,” there is one important decision you must make should you choose a Regular Plan or a Direct Plan?

This choice may seem small, but it can affect your final wealth by lakhs of rupees over time. More importantly, it affects your peace of mind, your ability to stay invested during market ups and downs, and the quality of guidance you receive.

At www.futuresavings.in, we are AMFI-registered distributors. We believe in honest, simple explanations. This guide will help you understand the difference clearly, so you can decide what is best for your own financial journey.

What is a Direct Plan?

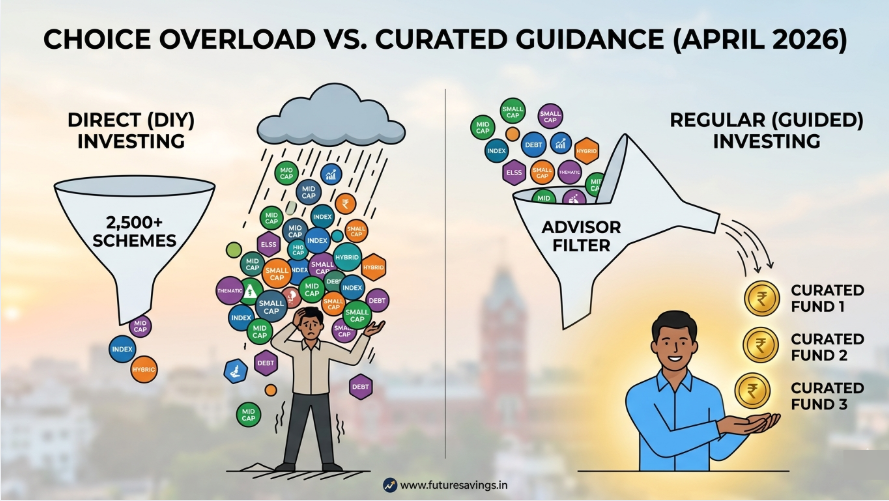

A Direct Plan means you buy mutual fund units directly from the Asset Management Company (AMC). You do not take help from any distributor or advisor. You choose the fund yourself, you decide when to invest, and you manage everything on your own.

Key points about Direct Plans:

- Lower expense ratio (typically 0.5% to 1% less than Regular plans)

- Higher NAV over time because no professional fees are paid

- You are fully responsible for research, selection, timing, and tax planning

- No one to guide you during market falls or crashes

A Direct Plan is suitable only for those who have good knowledge of mutual funds, enough time to monitor their portfolio regularly, and the emotional discipline to not panic during market volatility.

What is a Regular Plan?

A Regular Plan means you invest through a AMFI-registered distributor, or advisor, or financial planner. You do not go directly to the AMC. Instead, a professional helps you at every step from selecting the right funds to monitoring your portfolio and keeping you on track.

Key points about Regular Plans:

- Slightly higher expense ratio (0.5% to 1% more than Direct plans)

- This extra amount pays for expert advice, portfolio monitoring, and emotional guidance

- Your advisor handles paperwork, KYC updates, nominations, and tax harvesting

- You have someone to call when markets crash and you feel scared

For most investors especially those who are busy, new to investing, or have specific life goals a Regular Plan offers better overall value and a higher chance of success.

Why Does This Choice Matter in 2026?

The year 2026 is different from previous years. The market is experiencing elevated volatility and moderating valuations. This means prices are no longer cheap, and ups and downs will be sharper.

In such an environment, the biggest risk is not the expense ratio. The biggest risk is your own behaviour.

Key point:

A Direct Plan saves you money on fees, but a Regular Plan saves you from yourself.

When markets crash, a Direct Plan investor is alone with their fear. Many sell at the bottom and lose years of gains. A Regular Plan investor has an advisor to call someone who will say, “Stay calm & why? This is temporary or permanent? Time to sell or do not sell. Why & how & when?

That single phone call can save you more money than you would ever save by choosing a Direct Plan.

Who Should Choose a Direct Plan?

A Direct Plan works well if you answer “yes” to most of these questions:

- Do you enjoy reading mutual fund documents and tracking returns on Excel?

- Do you stay calm when your portfolio shows a 10-15% loss?

- Are you comfortable managing your own KYC, nominations, and tax filings?

- Do you have several hours every month to research and monitor your investments?

If yes, then a Direct Plan is a good choice for you. You have the knowledge, time, and temperament to go alone.

Who Should Choose a Regular Plan?

A Regular Plan is better if you answer “yes” to any of these questions:

- Are you a busy professional (doctor, engineer, business owner) with limited time?

- Are you new to investing and still learning the basics?

- Do you have specific financial goals like children’s education or retirement?

- Would you prefer to sleep peacefully knowing a professional is watching your money?

- Do you want someone to handle paperwork, tax harvesting, and portfolio rebalancing?

If yes, then a Regular Plan is likely the better choice for you. You are not paying only for returns you are paying for guidance, discipline, and peace of mind.

The Cost Difference: A Simple Explanation

Let us talk about money directly. The difference in expense ratio between a Direct Plan and a Regular Plan is about 0.75% on average.

Example:

If you invest Rs 10,000 per month for 20 years at 10% returns, the difference between Direct and Regular could be around Rs 7 lakh in final corpus.

That sounds like a lot. But here is what most people forget.

Hidden costs of Direct Plans:

- Tax harvesting miss: Most Direct investors forget to do tax harvesting. This can cost Rs 4 to 5 lakh in lost tax savings over 20 years.

- Panic selling: One wrong decision during a crash can cost 10-15% of your portfolio. On a Rs 50 lakh portfolio, that is Rs 5 – 7.5 lakh lost.

- Wrong fund selection: If you pick a fund that underperforms by 2%, you lose far more than you save in expenses.

- Time cost: Managing your own portfolio takes 5-10 hours every month. What is your time worth?

When you add all these hidden costs, the Regular Plan often comes out ahead for the average investor.

The Hidden Value of Regular Plans (As a Distributor, We See This Every Day)

Because we work with investors every day, we see the real value of Regular Plans. It is not just about returns. It is about these five things.

1. You stay invested longer.

The single biggest factor in wealth creation is time in the market. A good advisor prevents you from making emotional exits. You stay invested, and compounding does its magic.

2. You avoid performance chasing.

Most investors buy funds that have done well recently. By then, it is often too late. An advisor keeps you focused on long-term consistency, not past winners.

3. You get tax harvesting done automatically.

Every year, you can save up to Rs 1,25,000 in taxes by harvesting long-term capital gains. An advisor does this for you. Most Direct investors forget.

4. You have someone to call during a crisis.

When markets crash, fear is real. Having a professional to talk to prevents you from making expensive mistakes. This alone is worth more than the extra expense ratio.

5. Your family is protected.

If something happens to you, your advisor helps your family claim all investments. With Direct plans, families often struggle to find and recover the money.

A Slight but Honest Advantage of Regular Plans

We are distributors and advisors. We will not pretend to be neutral. We believe that for the majority of investors, a Regular Plan offers a higher probability of success.

Why? Because investing is not 100% mathematics. It is 90% behaviour and 10% numbers. A Regular Plan fixes your behaviour.

Think of it this way:

You can cut your own hair and save money. But most people go to a professional because the result is better. Similarly, you can file your own taxes, but most people hire an accountant to avoid mistakes. Investing is no different.

A Direct Plan is like driving alone on a highway. A Regular Plan is like having a co-driver with a map. Both can reach the destination. But one is less stressful, safer, and more likely to arrive on time.

If you are a true expert with iron discipline, go Direct. If you are like most people busy, human, and emotional then go Regular.

Conclusion

The choice between Regular and Direct is personal. There is no single right answer for everyone.

| Your Situation | Better Choice |

| Investing is your hobby. You enjoy research. | Direct |

| You never panic during market falls. | Direct |

| You have time to manage everything yourself. | Direct |

| You want someone to handle paperwork and tax planning. | Regular |

| You are busy with your career or business. | Regular |

| You want peace of mind and professional guidance. | Regular |

In 2026, with market volatility and moderating valuations, having a professional in your corner is a strategic advantage. The Direct route offers a lower price. The Regular route offers a higher probability of reaching your goals peacefully.

Ready to Start Your Journey?

Whether you choose the self-reliant path or the guided route, the most important step is to begin.

Explore more resources at www.futuresavings.in to find the best mutual funds for your specific goals.

Disclaimer: Mutual Fund investments are subject to market risks. Please read all scheme-related documents carefully before investing. Past performance does not guarantee future returns.

Leave A Comment