Empowering your journey to financial success

with every milestone achieved.

Systematic Investment Plan: A Complete Guide

Table of Contents

Did you know over 6.5 crore Indians are already running a SIP right now? That’s more than the entire population of France, investing every single month. But here’s the uncomfortable truth, most of them don’t know what they’re actually building towards. They started because someone told them to. Not because they had a goal. If you’ve been putting off investing because it feels complicated, confusing, or “something to figure out later” you’re not alone. Inflation is quietly eating your savings. Salaries are rising, but so are expenses. And with the updated tax slabs under the Income Tax Act 2026, the cost of not investing has never been higher.

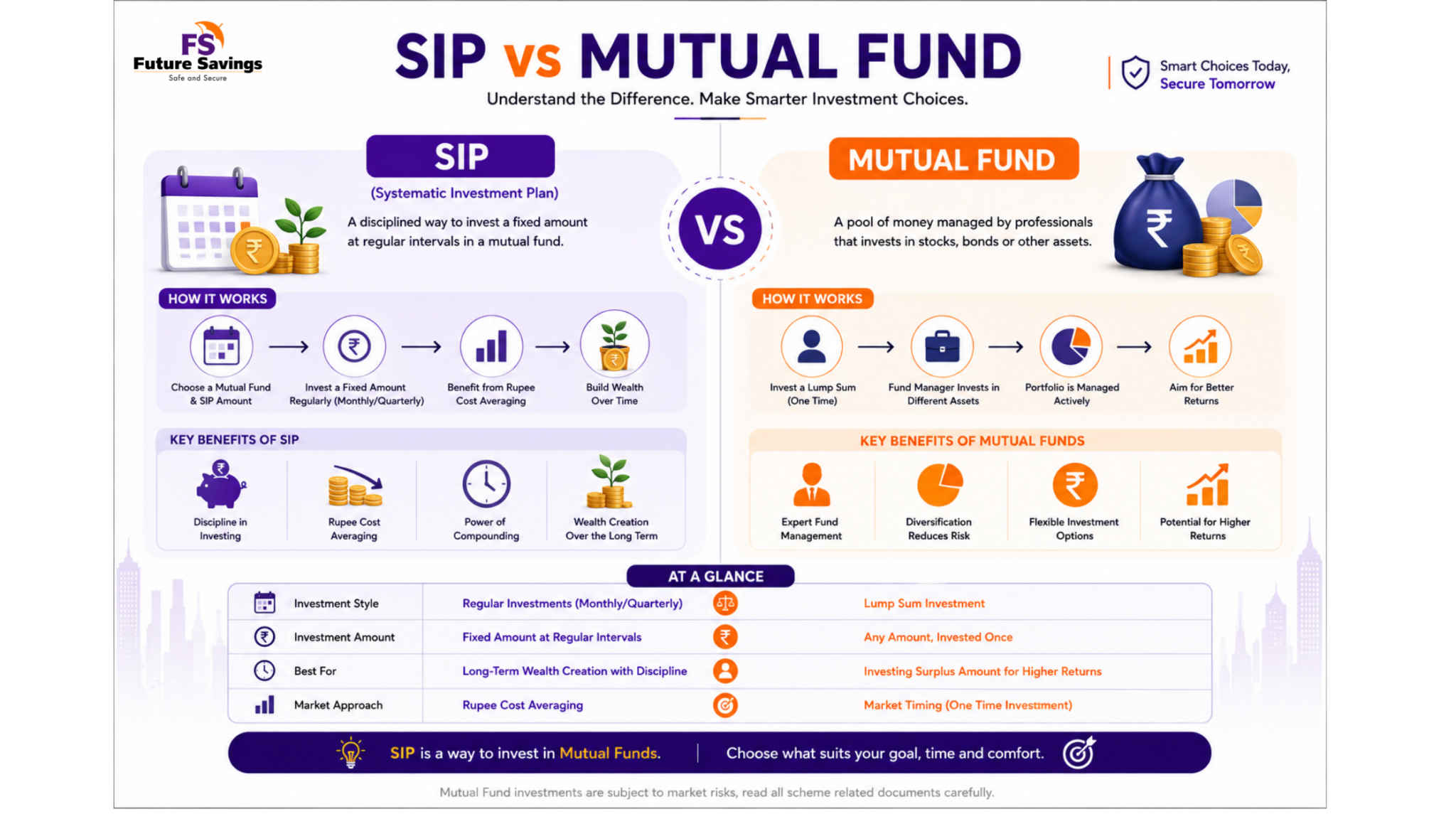

What Exactly is a SIP? (It’s Not a Mutual Fund) :

SIP stands for Systematic Investment Plan. Let’s break that down:

- Systematic – fixed, regular, automatic

- Investment – your money going to work

- Plan – a method, not a product

A SIP is not a mutual fund. It’s the way you invest in one like how UPI AutoPay is not Netflix, it’s just how you pay for it.

Think of it this way: A SIP is to mutual funds what an EMI is to your home loan. The EMI doesn’t own your house, it’s just the disciplined method that gets you there.

So what is a mutual fund? It’s a pool of money collected from thousands of investors, managed by a professional fund manager, and invested across a basket of market-linked instruments. Every time your SIP instalment goes in, you’re buying units at that day’s NAV ( Net Asset Value), simply the current price of one unit.

You don’t need to watch the market. You don’t need to time anything. The SIP invests on your chosen date, rain or shine.

SIP investments are popular because they reduce the pressure of timing the market. Beginners often feel anxious about when to invest. With SIPs, investments happen automatically at fixed intervals, regardless of whether markets are rising or falling. This approach may help smooth out market volatility through rupee cost averaging.

Another reason SIPs have gained traction is accessibility. Many investment platforms now allow SIPs starting from ₹500 per month. This makes investing more approachable for young professionals, freelancers, and first-time investors who may not have large surplus capital available initially.

How Does a SIP Actually Work?

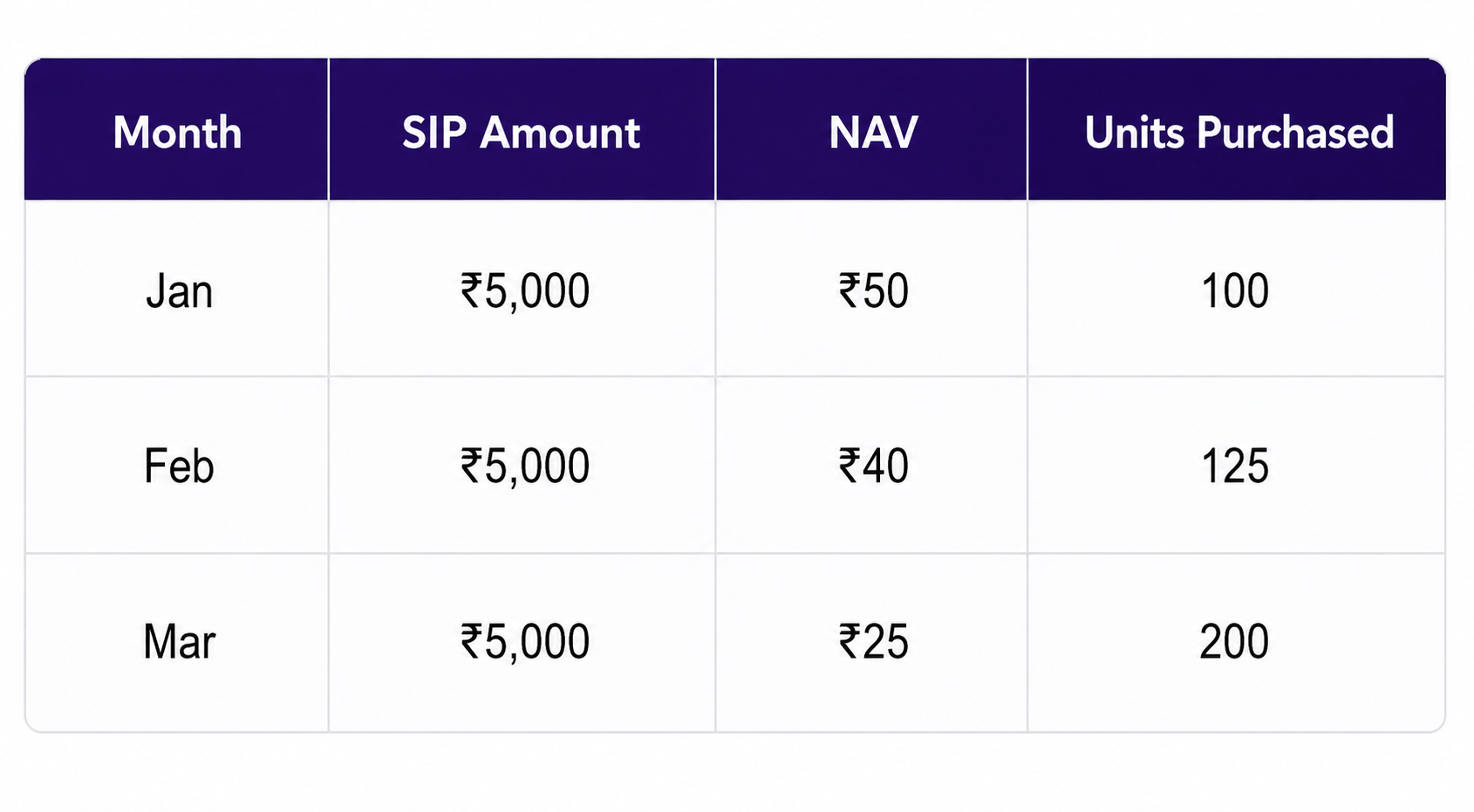

A SIP follows a simple recurring investment structure. Once you select a mutual fund category and decide your investment amount, your bank account gets automatically debited on a chosen date every month. In return, you receive mutual fund units based on the fund’s current NAV, also called Net Asset Value.

For example, if your SIP amount is ₹5,000 and the NAV of the scheme is ₹50, you receive 100 units. If the NAV drops to ₹25 the following month, your ₹5,000 buys 200 units instead. Over time, this process is known as rupee cost averaging. It helps distribute investment costs across different market levels rather than relying on a single entry point.

Note: Investors should also remember that different mutual fund categories carry different levels of risk and volatility.

Why SIPs are Perfect for early Indian Investors in 2026

In 2026, SIP investments continue to attract young investors because they align naturally with monthly income cycles and long-term wealth-building behavior.

Most salaried professionals receive income monthly. Freelancers and business owners may also prefer smaller, disciplined contributions rather than large one-time investments. SIPs fit this structure well because they encourage investing consistency without requiring a huge initial commitment. Even a modest SIP amount, when invested regularly over many years, may accumulate into a meaningful corpus depending on market performance and investment duration.

Another important factor is inflation. The cost of education, healthcare, travel, and housing has increased steadily over time. Keeping money idle in low-growth instruments may not always support long-term wealth creation goals. SIP investments allow investors to participate in market-linked growth opportunities while spreading investment risk over time.

During market volatility, investors often panic and make emotional decisions. Automated investing helps reduce this tendency because investments continue irrespective of short-term market fluctuations. This consistency is one reason SIPs remain popular among first-time investors.

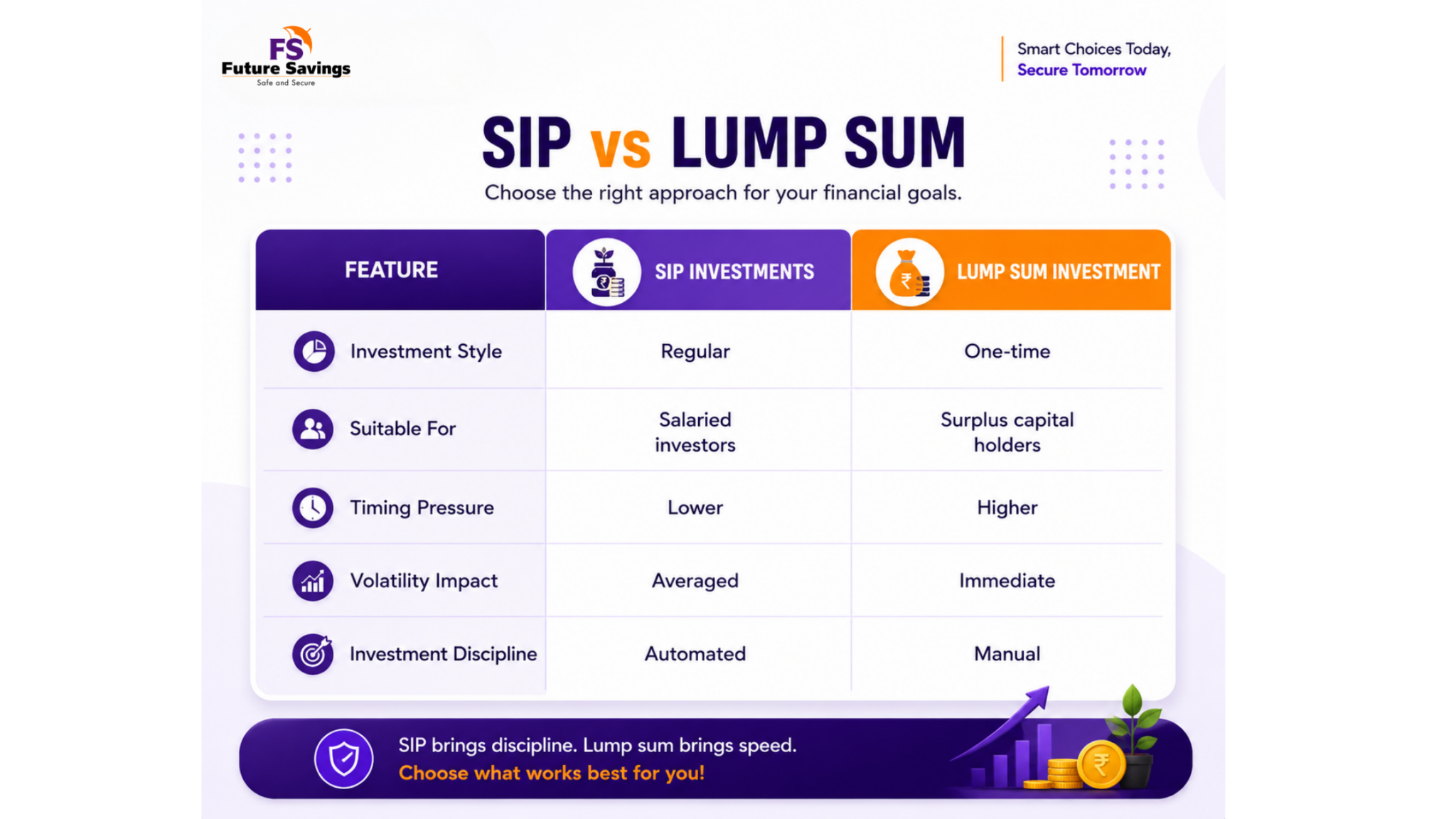

SIP vs Lump Sum: Which Should You Choose?

Many First time investors ask whether SIP investments are better than lump sum investing. The answer depends entirely on your financial situation, cash flow, risk tolerance, and investment goals. Both methods have advantages and limitations, and neither approach is universally superior for every investor.

A SIP involves investing smaller amounts regularly over time. This method is generally preferred by salaried individuals, freelancers, and first-time investors because it reduces the emotional pressure of market timing.

Lump sum investing, on the other hand, involves investing a large amount at one time. This approach may suit investors who receive bonuses, inheritance, business profits, or other large cash inflows.

How Much Should You Invest?

There is no perfect SIP amount that works for everyone. The ideal investment amount depends on your income, expenses, financial goals, risk appetite, liabilities, and investment timeline. In reality, consistency matters more than starting big.

A practical approach many investors follow is allocating a percentage of monthly income toward long-term investing goals. For some individuals, this may be 10% of income, while others may invest more depending on financial stability and future goals. The key is choosing an amount that feels sustainable over the long term without disrupting essential expenses or emergency savings.

Different goals require different investment horizons. Short-term goals may require relatively conservative approaches, while long-term goals may allow more exposure to growth-oriented market-linked investments.

One powerful strategy beginners should understand is the Step-Up SIP. This feature allows investors to increase SIP amounts annually. Even a 10% increase every year may significantly improve long-term wealth accumulation depending on market conditions and investment duration.

5 SIP Mistakes Beginners Make (And How to Fix Them)

- Random Investing: One of the most common mistakes is investing without a clear financial goal. Random investing often leads to inconsistent contributions and emotional decisions. Investors should ideally connect every SIP to a specific objective such as retirement, child education, or emergency planning.

- stopping SIPs during market corrections: Another major mistake is stopping SIPs during market corrections. Market volatility is a normal part of equity-oriented investing. Historically, investors who remained disciplined during fluctuations often benefited from long-term participation, although future performance is never guaranteed. Panic-based exits may disrupt long-term wealth-building plans.

- Rely heavily on social media trends: Many beginners also rely heavily on social media trends or “highest return” discussions without understanding suitability or risk levels. Chasing performance alone may create unrealistic expectations. Investors should instead focus on asset allocation, investment horizon, and personal financial goals.

Ignoring important scheme documents is another issue. Before investing, investors should read:

- SID (Scheme Information Document)

- KIM (Key Information Memorandum)

- Riskometer

- Expense ratio details

Lastly, many people fail to review SIPs regularly. Income levels, goals, and risk profiles evolve over time. Annual portfolio reviews with qualified advisors may help maintain better alignment between investments and life goals.

How to Start Your First SIP in 2026:

- Starting a SIP in India has become significantly easier due to digital investment platforms and paperless KYC systems. Most investors can now complete the process online within a few minutes. However, beginners should focus not only on convenience but also on suitability and compliance.

- The first step is completing KYC verification using PAN, Aadhaar, mobile number, and bank account details. Once verification is complete, investors should identify their financial goals and investment horizon. Choosing a fund category should depend on suitability rather than short-term return expectations.

- After selecting the SIP amount and investment frequency, investors can activate auto-debit mandates through ECS or NACH systems. Automated investing encourages consistency and reduces missed contributions.

That’s where Futuresavings follows a goal-first approach instead of pushing random investment products. The focus is on helping investors understand why they are investing before deciding where to invest.

Book Your Free SIP Consultation with our Financial Experts

When SIP Isn’t Enough: Why Smart Investors Upgrade to Wealth Management

SIP investments are often the first step toward financial planning, but long-term wealth creation usually requires a broader strategy. As income grows and financial responsibilities increase, investors may eventually need more structured financial planning support. This is where wealth management becomes relevant.

Over time, they may also require:

- Tax-efficient investing strategies

- Insurance planning

- Asset allocation guidance

- Business cash flow planning

- Retirement income structuring

- Family financial protection planning

This becomes especially important for first time investors, entrepreneurs, and high-income professionals with complex financial situations.

At Futuresavings, the focus remains on personalized financial planning and disciplined long-term investing behavior. Instead of promoting specific funds or products, the emphasis stays on understanding investor goals, time horizons, liquidity needs, and risk tolerance.

Professional guidance may also help investors avoid emotional decisions during volatile markets and maintain better financial discipline over time.

Conclusion :

SIP investments continue to remain one of the most accessible entry points for beginner investors in India in 2026. They simplify investing, encourage discipline, and help investors participate in long-term market-linked growth opportunities without requiring large starting capital. However, successful investing is not about blindly starting a SIP and forgetting it. It requires goal clarity, consistency, periodic review, and alignment with changing financial needs.

Whether your objective is retirement planning, wealth creation, child education, or financial independence, SIPs may support long-term progress when used thoughtfully and consistently. Investors should always evaluate suitability, understand risks, and avoid performance-based decision-making without proper planning.

If you’re looking for a personalized, goal-first investing roadmap instead of generic investment advice, explore Futuresavings Wealth management service Consultation today.

Guide to SIP: Frequently Asking Questions

1. What is a SIP in mutual funds?

A SIP, or Systematic Investment Plan, is a method of investing a fixed amount regularly into a market-linked mutual fund scheme. It helps investors invest consistently without needing to time the market. A SIP itself is not a mutual fund or guaranteed-return product.

2. How much money do I need to start a SIP in India?

Many investment platforms in India allow SIP investments starting from ₹500 per month. The ideal amount depends on your income, financial goals, and investment horizon. Beginners often start small and gradually increase contributions through Step-Up SIPs.

3. Are SIP investments risk-free?

No. SIP investments are market-linked because they invest in mutual funds. The value of investments may go up or down depending on market conditions and fund performance. Returns are not guaranteed.

4. Can I stop or pause my SIP anytime?

Yes. Most SIPs can be paused, modified, or stopped anytime through the investment platform or AMC portal, depending on scheme terms and platform policies. However, stopping investments frequently may affect long-term financial goals.

5. What is the difference between SIP and lump sum investment?

A SIP involves investing smaller amounts regularly, while lump sum investing means investing a large amount at once. SIPs may help reduce the impact of market volatility through rupee cost averaging, whereas lump sum investments are more exposed to market timing risk.

6. How long should I continue SIP investments?

The duration depends on your financial goals. Long-term goals like retirement or child education often require investment horizons of 10 years or more. Historically, longer investment periods have helped reduce the impact of short-term market volatility, though returns are not guaranteed.

7. What is a Step-Up SIP?

A Step-Up SIP allows investors to increase their SIP amount periodically, usually every year. This feature may help align investments with salary growth, inflation, and increasing financial goals over time.

8. Is SIP better than a fixed deposit (FD)?

SIPs and fixed deposits serve different purposes. Fixed deposits generally offer fixed interest rates, while SIP investments are market-linked and may offer long-term growth potential depending on market conditions. SIP returns are not fixed or guaranteed.

9. Are SIP investments eligible for tax benefits?

Certain mutual fund categories like ELSS (Equity Linked Savings Scheme) may qualify for tax deductions under Section 80C up to the applicable limit under FY 2025-26 / AY 2026-27 rules. ELSS investments come with a mandatory 3-year lock-in period.

10. How can Futuresavings help beginners start SIP investments?

Futuresavings follows a goal-first approach to help beginners understand investment planning instead of chasing random market trends. Contact us for more personalized services in investments.

Realted Blogs on Mutual Funds

- On April 15, 2026

Understanding Lump Sum Investing

Read now

Financial Planning Investment Mutual Funds Wealth Management

- On April 15, 2026

Systematic Transfer Plan (STP)

Read now

Financial Planning Investment Mutual Funds Wealth Management

- On April 15, 2026

Understanding SIP

{kind=link}

{kind=link}

{kind=link}