(STP): The “Sleep Well at Night” Strategy

How to Move Big Money Without the Big Risk | www.futuresavings.in

You just received a windfall maybe it’s a Rs10 Lakh bonus, a property sale, or an inheritance. You know you should put it in the stock market, but your gut is screaming: “What if the market crashes tomorrow?”

This fear is real, and it’s the 1 reason big money stays idle in savings accounts, losing value to inflation every day. At Future Saving, we use the STP to kill that fear.

1. What is an STP?

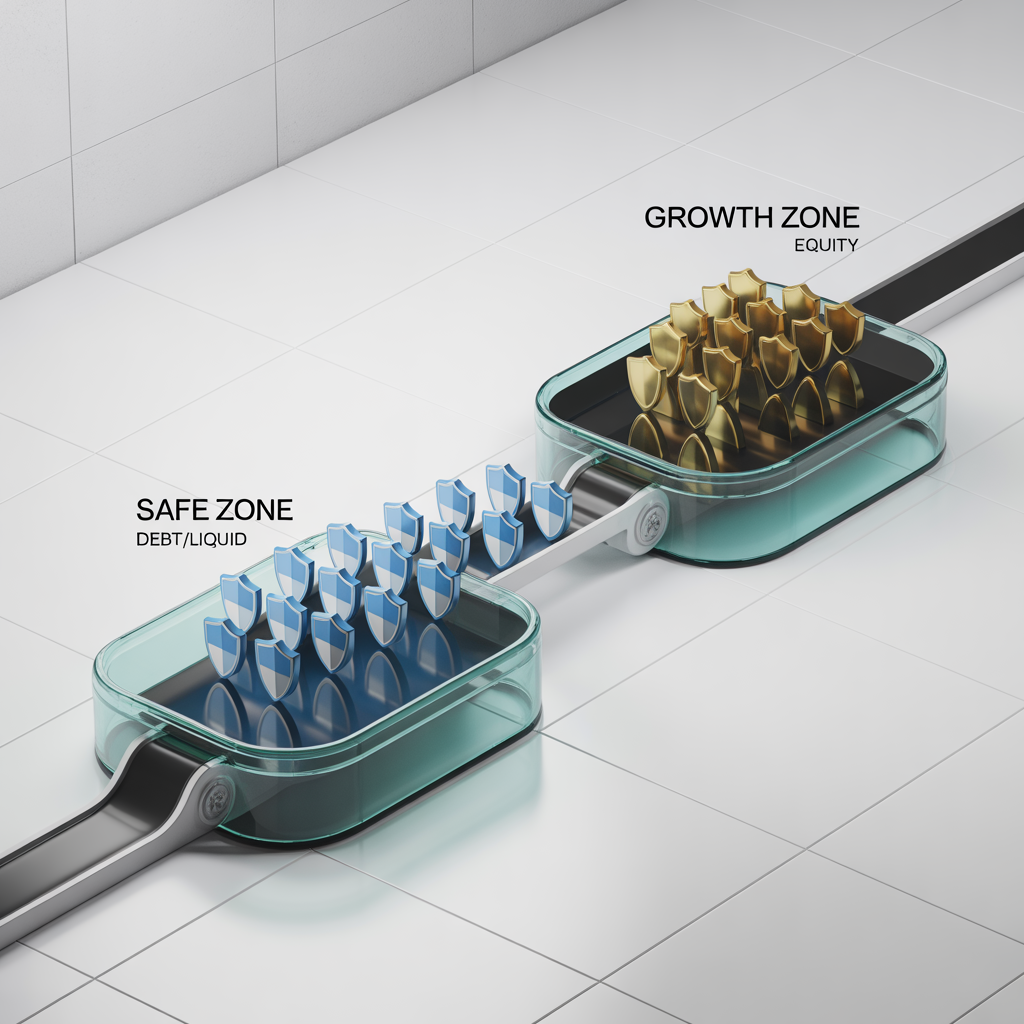

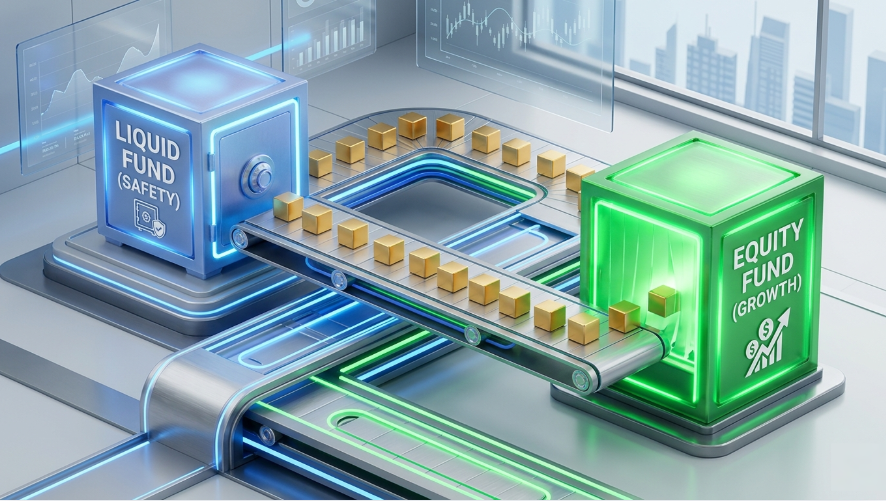

An STP isn’t a fund; it’s a conveyor belt.

It allows you to park your large pile of cash in a safe, boring place (Source) and automatically move a small piece of it into a growth-oriented place (Target) every month.

- The Source: A low-risk Debt or Liquid Fund (Like a secure parking lot).

- The Target: An Equity Mutual Fund (Like a high-speed highway).

2. Why Choose STP?

If you invest Rs10 Lakhs as a Lump Sum and the market drops 10% next week, you lose Rs1 Lakh instantly. That hurts.

With an STP, if the market crashes next week, only your first instalment (say Rs50,000) is affected. The remaining Rs9.5 Lakhs is sitting safely in your debt fund, earning interest and waiting to buy those equity units at a massive discount next month.

The STP Mantra: It’s not about beating the market; it’s about eliminating regret.

3. How it Works: The Conveyor Belt in Action

Imagine you have Rs6,00,000. You’re nervous, so you set up a 12-month STP:

- Day 1: You drop the full Rs6 Lakhs into a Liquid Fund. It starts earning 6-7% interest immediately.

- Every Month: The “belt” moves Rs50,000 into your Equity Fund.

- The Result: By the end of the year, your money is fully invested in equity, but you bought in at 12 different price points. You’ve “averaged” your risk while your idle cash was still working for you.

4. The Benefits: Why We Love It

- Risk Mitigation: You never “buy the peak” with your whole portfolio.

- Idle Money Growth: Your money earns more in a Liquid Fund than a 3% savings account while it waits its turn.

- Emotional Discipline: You don’t have to watch the news. The transfer happens automatically, whether the market is “bleeding red” or “roaring green.”

- Rupee Cost Averaging: You buy more units when they are cheap and fewer when they are expensive.

5. The Math: XIRR (The Real Truth)

Since your money is entering the equity fund in “waves,” you can’t use a simple percentage to calculate returns. We use XIRR (Extended Internal Rate of Return).

It considers:

- The interest earned in the safe fund.

- The growth of each staggered instalment in the equity fund.

Note: Most investors find that while an STP might have slightly lower returns than a perfectly timed Lump Sum, it almost always has higher returns than a poorly timed one.

6. When to Trigger an STP?

- Windfalls: Bonus, inheritance, or asset sales.

- Market Highs: When the Nifty/Sensex looks “expensive” but you don’t want to miss out entirely.

- Low Risk Tolerance: If seeing a 10% drop on your screen makes you want to sell everything.

Disclaimer: Mutual Fund investments are subject to market risks.

Read all scheme-related documents carefully.

Leave A Comment