Which Path Leads to True Wealth?

In the fast-evolving financial landscape of April 2026, investors are more empowered than ever. With a simple tap on a smartphone, you can access the best Mutual Funds in the country. However, before you click “Invest,” you are faced with a critical choice that will dictate your financial journey for the next decade: Regular vs. Direct.

At www.futuresavings.in, we believe that the “cheapest” option isn’t always the “best” option. In this guide, we break down the nuances of these two paths to help you decide which one aligns with your life goals.

1. WHAT is the Difference?

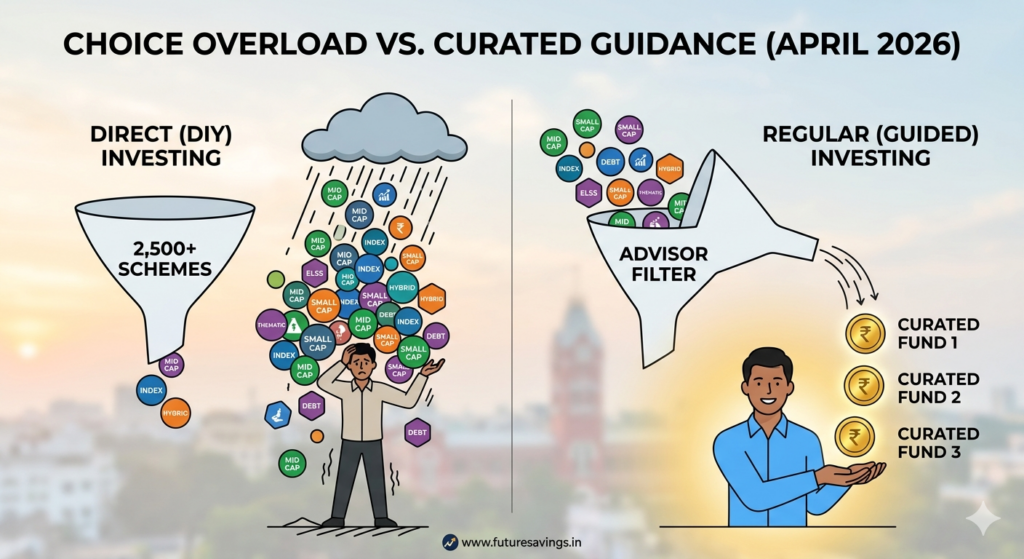

What is Direct?

A Direct Plan is an investment route where you buy units directly from the Asset Management Company (AMC). There are no intermediaries, agents, or brokers involved.

- The Key point: Because the AMC doesn’t have to pay a commission to anyone, they charge a lower Expense Ratio.

- The Result: This results in a slightly higher Net Asset Value (NAV) over time.

What is Regular?

A Regular Plan is an investment made through a financial intermediary—be it a distributor, a bank, or a certified financial advisor.

- The Key point: You pay a slightly higher expense ratio (typically 0.5% to 1.0% more than direct).

- The Result: This extra cost is used to pay for the expertise, administrative support, and behavioural coaching provided by your advisor.

2. WHY does this choice matter in 2026?

With the current elevated volatility in the market and moderating valuations, the “gap” between a successful investor and an unsuccessful one isn’t just about the expense ratio; it’s about staying the course.

The Math of Direct

If you invest ₹10,000 monthly for 20 years, a 0.75% difference in expense ratio could result in a difference of several lakhs in your final corpus. For a disciplined, highly knowledgeable “DIY” (Do-It-Yourself) investor, this is “free money.”

The Psychology of Regular

Investing is 10% math and 90% temperament. In a Regular Plan, you aren’t just paying for a transaction; you are paying for a Shield. When markets crash (as they did during the recent geopolitical jitters of early 2026), a Regular Plan investor has an advisor to call. That advisor prevents the investor from making the #1 mistake in finance: Selling at the bottom.

3. WHO should choose which?

The “Direct” Persona:

- The Researcher: You enjoy reading 50-page SID (Scheme Information Documents) and tracking XIRR on Excel.

- The Emotionally Stoic: You don’t panic when your portfolio turns red.

- The Tech-Savvy: You are comfortable managing your own KYC, FATCA declarations, and nominee updates across multiple platforms.

The “Regular” Persona:

- The Busy Professional: You are a doctor, engineer, or entrepreneur. Your time is better spent earning in your profession than tracking the Nifty 50 every hour.

- The New Investor: You are just starting and need help understanding the Periodic Table of Mutual Funds.

- The Goal-Seeker: You want someone to remind you why you are investing (e.g., “This is for your daughter’s education, don’t touch it!”).

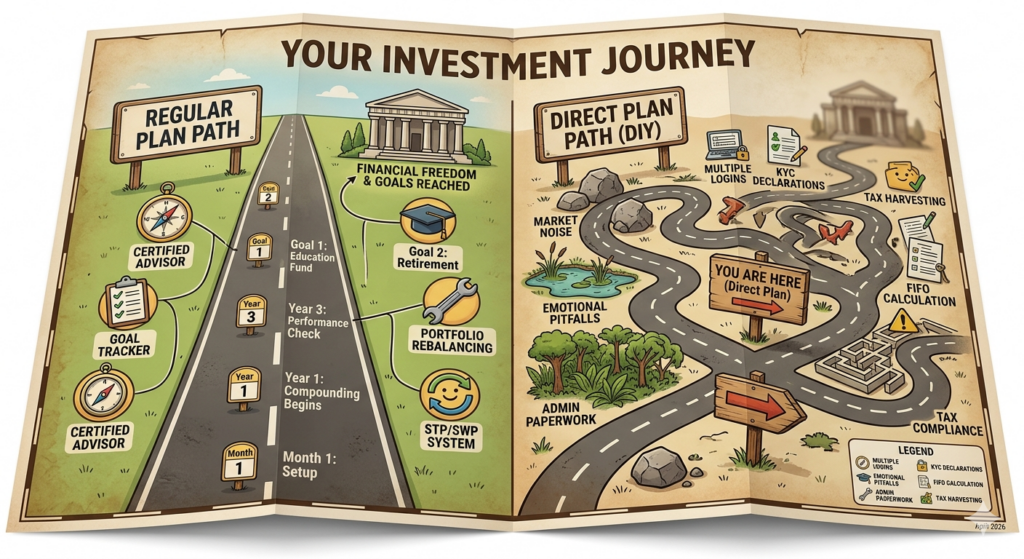

4. WHEN is the Time to Invest?

A common question we receive at www.futuresavings.in is: “When is the best time to invest?”

The answer is: Now. But the way you invest depends on your choice:

- In Direct: You must decide the “When” yourself. You must monitor if it’s the right time for Small Caps or if you should shift to Debt.

- In Regular: Your advisor manages the “When” through STP (Systematic Transfer Plans) and rebalancing, ensuring you enter the market at optimal valuations without the stress of timing it yourself.

5. HOW to Execute: The Pros and Cons

Pros & Cons of Direct Plans

| Pros | Cons |

| Lower Expense Ratio: More of your money is invested. | High Responsibility: You are liable for your own mistakes. |

| Higher Returns: Compounding works on a larger base. | No Support: You handle all paperwork and technical glitches. |

| No Bias: No one is “selling” you a fund for commission. | Emotional Traps: No one to stop you from panic-buying or selling. |

Pros & Cons of Regular Plans

| Pros | Cons |

| Expert Guidance: Access to the best Mutual Funds tailored to you. | Cost: Higher Expense Ratio reduces the “pure” return slightly. |

| Behavioural Coaching: Someone to keep you calm during volatility. | Incentive Risk: Some distributors might push funds with higher commissions. |

| Consolidated View: One person manages your family’s entire portfolio. | Performance Lag: Over 25 years, the cost gap becomes visible. |

6. The Deep Dive: Why Regular Often Wins the “Real” Race

Many financial influencers argue that “Direct is better because it’s cheaper.” But in the real world, the Regular vs. Direct debate isn’t about cost—it’s about Value.

A. The “Wrong Fund” Cost

If you choose a Direct plan but pick a fund that underperforms its benchmark by 2%, you have “saved” 0.75% on fees but “lost” 2% on performance. A Regular advisor’s primary job is to ensure you are in a fund that consistently beats the average.

B. The “Paperwork” Cost

Life happens. People move houses, change phone numbers, and lose track of old investments. A Regular advisor keeps your records clean. For many, the time saved on administrative headaches is worth more than the 1% fee.

C. The “Tax Harvesting” Edge

At www.futuresavings.in, we often discuss how to save tax. An advisor can help you execute “Tax Harvesting” (selling and buying to utilize the ₹1.25L LTCG limit). Most DIY investors forget to do this, losing more in taxes than they saved in Direct fees.

7. Final Verdict: The Future savings Perspective

The choice of Regular vs. Direct is personal.

- If you view investing as a hobby, go Direct.

- If you view investing as a necessity for your family’s future but don’t want it to consume your life, go Regular.

In 2026, where “Moderating Valuations” require a surgical approach to picking stocks, having a professional in your corner is a strategic advantage. While the DIY route offers a lower price, the Regular route offers a higher probability of reaching the finish line.

Ready to start your journey? Whether you choose the path of the self-reliant navigator or the guided traveller, the most important step is to begin. Explore more resources at www.futuresavings.in to find the best Mutual Funds for your specific goals.

Disclaimer: Mutual Fund investments are subject to market risks.

Read all scheme-related documents carefully before investing.

Leave A Comment