Table of Contents

- Overview: The Modern Way to Save

- Payment Modes: Making Investing “Auto-Pilot”

- The Twin Engines: Compounding and Rupee Cost Averaging

- Normal SIP vs. Step-Up SIP: The Growth Gap

- Comparison: Bank RD (6.5%) vs. Mutual Funds (13%)

- Conclusion

- FAQs

Overview: The Modern Way to Save

For decades, the Recurring Deposit (RD) was the go-to for Indian households. While safe, RDs often struggle to beat inflation. At Future Savings, we advocate for a more dynamic approach. Mutual Funds, through Systematic Investment Plans (SIPs), allow you to participate in India’s economic growth story with as little as Rs 500 per month. This guide explains how to turn small monthly sums into a significant financial legacy.

Payment Modes: Making Investing “Auto-Pilot”

In 2026, you no longer need to worry about physical checks or complex net banking logins every month. Modern payment modes have made investing seamless:

- UPI AutoPay: The most popular choice today. You set a one-time mandate on apps like Google Pay or PhonePe, and your SIP amount is deducted automatically.

- E-Mandate (Net Banking): A digital instruction to your bank to allow the AMC (Asset Management Company) to pull the SIP amount on a fixed date.

- NEFT/RTGS: Usually used for large, one-time (lumpsum) investments.

The Twin Engines: Compounding and Rupee Cost Averaging

Why do Mutual Funds work so well over time? It comes down to two mathematical “superpowers”:

- The Power of Compounding: This is “interest on interest.” As your investment earns returns, those returns are reinvested to earn even more. Over 10 years, the growth is not linear; it is exponential.

- Rupee Cost Averaging: You don’t need to “time the market.” When the market is down, your fixed SIP amount buys more units. When the market is up, it buys fewer units. Over time, your average cost per unit stays low, maximizing your gains when the market rises.

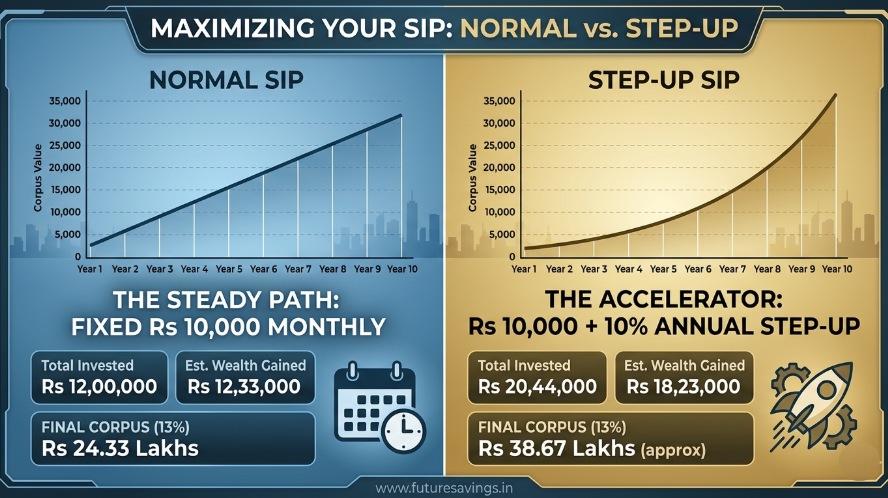

Normal SIP vs. Step-Up SIP: The Growth Gap

A Normal SIP is a fixed amount (e.g., Rs 10,000) every month.

A Step-Up SIP (or Top-Up SIP) increases your contribution annually (e.g., by 10 percent) to match your salary hikes.

Example (10-Year Period at 13% Returns):

- Normal SIP: Rs 10,000 every month.

- Step-Up SIP: Starts at Rs 10,000, but increases by 10% every year.

By the end of year 10, the Step-Up investor has contributed more, but the final corpus is significantly larger because the “stepped-up” amounts also began compounding immediately.

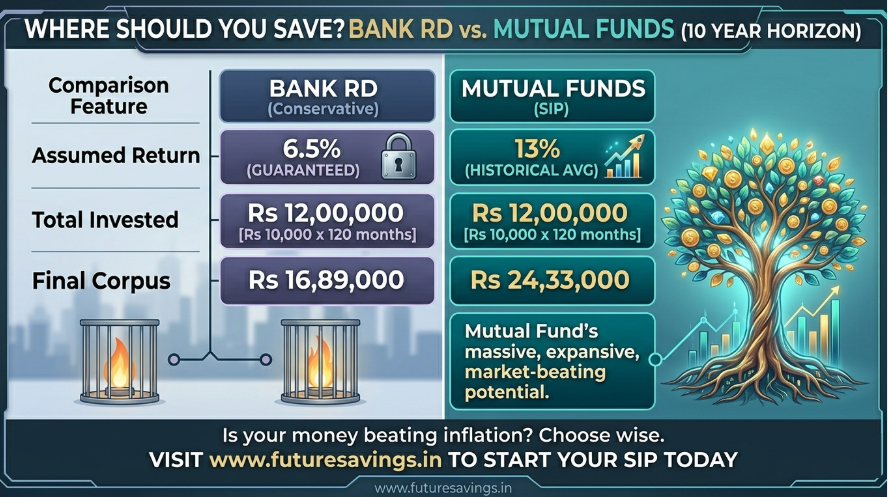

Comparison: Bank RD vs. Mutual Funds (10-Year Horizon)

Let’s look at the numbers. We compare a monthly investment of Rs 10,000 over 10 years.

| Feature | Bank RD (Conservative) | Mutual Fund SIP (Aggressive) |

| Assumed Annual Return | 6.5% | 13% |

| Monthly Investment | Rs 10,000 | Rs 10,000 |

| Total Invested (10 Yrs) | Rs 12,00,000 | Rs 12,00,000 |

| Estimated Wealth Gained | Rs 4,89,000 | Rs 12,33,000 |

| Final Corpus Value | Rs 16,89,000 | Rs 24,33,000 |

Note: Mutual fund returns are subject to market risks and are not guaranteed like RDs. However, historically, diversified equity funds in India have delivered 12-15% over long horizons.

Conclusion

The difference of nearly Rs 7.5 Lakhs in the table above is the “cost of waiting” or staying too conservative. While RDs have their place for short-term goals, long-term wealth is built in the equity markets. By using tools like UPI AutoPay and Step-Up SIPs, you ensure that your Future Savings keep growing even while you sleep.

FAQs

Q: Can I stop my SIP if I have a financial crisis?

A: Yes. Unlike an RD, which may have premature withdrawal penalties, you can “Pause” or “Stop” a Mutual Fund SIP at any time with no penalty.

Q: Is 13% return guaranteed in Mutual Funds?

A: No. Mutual funds do not offer fixed returns. 13% is a historical average for equity funds in India. Some years may be negative, while others may be 20% or more.

Q: Is UPI AutoPay safe for large SIP amounts?

A: Yes. UPI AutoPay is regulated by NPCI and uses the same high-level encryption as your regular UPI transactions. You can also set a maximum limit on the mandate for added safety.

Q: What is the tax on Mutual Fund gains?

A: As of 2026, for Equity Funds, Long Term Capital Gains (LTCG) over Rs 1.25 Lakhs per year are taxed at 12.5%. Short-term gains (under 1 year) are taxed at 20%.

Ready to start your journey? Calculate your future corpus today at www.futuresavings.in.

Leave A Comment